Rent prices have fallen drastically in Ontario and Landlords have felt the hit hard. Many rental units are on the market for prolonged periods of time while they remain vacant. According to Renters.ca December 2020 Rent Report Toronto’s rents were down 20 percent, year-over-year, in November 2020. Let’s look at these numbers in detail and see what options Landlords have.

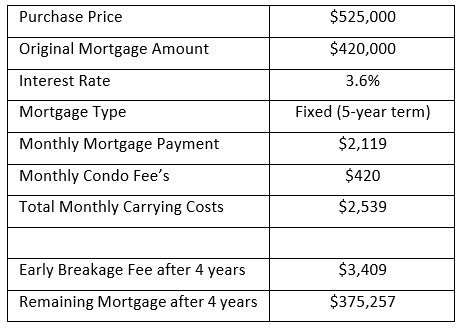

Let us take an example where a Landlord purchased a condo to rent for $525,000 four years ago and had put down 20 percent. Last year they were renting the condo unit for $2,200 a month, but it is now vacant for 2 months. They are potentially holding out for a higher rental amount. Their mortgage and overall carrying costs might look something like the graph below:

With a refinance Landlords have a few options. Let us look at three examples; refinance at a lower interest rate and pay off their mortgage quicker, refinance with low-interest rates and reduce the monthly out-of-pocket carrying costs and lastly use built-up equity and take advantage of the low-interest rates.

At the beginning of last year, this Landlord was only out of pocket $339 a month but was probably banking that the property value would go up and that the out-of-pocket amount would go directly to the principal.

Now with the new market, things have changed drastically. They are paying the same carrying costs but their new expected rental income is $1,760 (20% lower than the year prior). When the Landlord rents the unit out, the Landlord is out of pocket $779 a month. A difference of an extra $440 a month or $5,280 a year. For argument’s sake, let us say the new Condo value is $600,000 after these four years. With the current inventory of condo units on the market, the landlord would probably take a loss if they were to sell now.

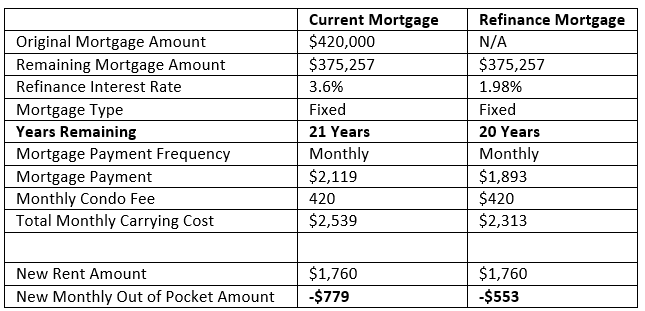

Option 1: Refinance & Pay-off Quicker

This option is where the Landlord has owned the unit for four years and could now take advantage of the lower interest rates and reduce their monthly carrying costs while being mortgage-free 1 year sooner.

The landlord will be mortgage-free 1 year earlier which saves tens of thousands of dollars and still have a lower out-of-pocket amount of $226 a month which would save $2,712 in the first year. Furthermore, more would go towards the principal and reduce the amount paid towards interest.

Key Benefits:

- Lower Your Monthly Mortgage Payments & Reduce Out-of-Pocket-Amount

- Pay Less in Interest & More Towards Principal

- Be Mortgage-Free Sooner & Save Tens of Thousands of Dollars

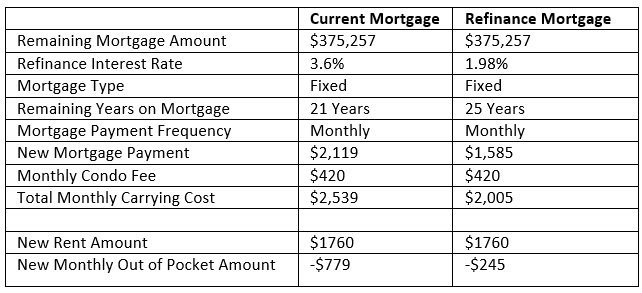

Option 2: Refinance & Reduce Out-of-Pocket Carrying Costs

This next option is where the Landlord will have a significantly lower monthly mortgage payment and reduce the unit’s carrying cost while making more payment towards the principal and less towards interest.

The Landlord will reduce the carrying costs of the unit by $534 a month which would save approximately $6,408 a year. Furthermore, reduce the monthly interest from approximately $1,136 to $617 which is another savings of approximately $519 a month and a total of $6,228 a year.

Key Benefits:

- Lower Your Monthly Mortgage Payments

- Reduce Out-of-Pocket-Amount

- Pay Less in Interest & More Towards Principal

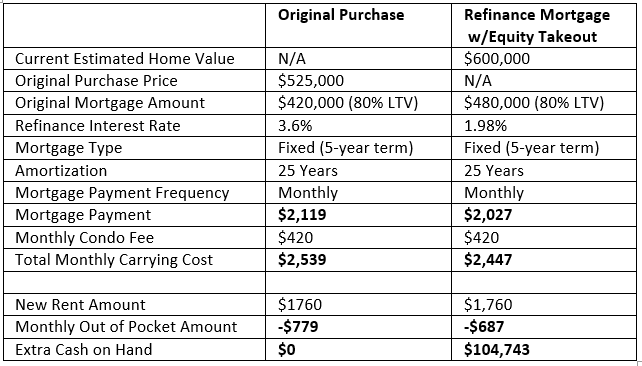

Option 3: Refinance & Equity Takeout

The example below allows the landlord to use some equity in the home and create a financial cushion. A landlord can borrow up to 80% loan to value (LTV) with a refinance, meaning they can borrow up to 80% of the value of the unit. We will consider 4 years have passed since the Landlord first purchased the property. This example may look like the below breakdown.

This example shows that the Landlord would have a lower payment amount and over one hundred thousand dollars in cash to do what they wish. He or she would have a lower out of pocket amount than they started with. This option will increase the amount towards the principal and reduce the amount towards interest.

Key Benefits:

- Lower Monthly Mortgage Payments

- Lower Monthly Out of Pocket Amount

- Have Extra Cash in Hand

All these numbers can get overwhelming, but a Mortgage Agent can help you. Not everyone’s savings would be like the above examples. They could be lower or higher, but with historically low mortgage rates, Landlords still have options. Speaking to a Mortgage Agent about possible options can save Landlords significant amounts of money and help them to reduce the burdens of declining rental prices.

It is important for Landlords to know they can still navigate these difficult times and still try and keep what they have spent so long to build up to.

Mortgage rates are at all-time lows and banks and lenders have made it simple for you to transfer your mortgage from one lender to another. This just means that you have options. When you deal directly with a bank, that bank is only able to offer you their options that they have in-house. A Mortgage Agent cannot only work to get you a mortgage at a bank, but they also work with multiple banks and other Grade A lenders. This is important because not only can they assist in saving you money with lower rates but also saving you money depending on your circumstances. There are multiple things outside of just the best rate and speaking with a Mortgage Agent can assist and protect your interests.

You are not guaranteed to save money or even qualify for a mortgage but you have a lot to gain, so speaking with a mortgage agent will benefit you.

#10390